Financial Brand Valuation:

A Semiotic Approach to Link Marketing and Finance

Paulo de Lencastre, Catholic University of Portugal, Porto, Portugal, plencastre@porto.ucp.pt

Nuno Côrte-Real, Catholic University of Portugal, Porto, Portugal, ncortereal@porto.ucp.pt

Ana Côrte-Real, Catholic University of Portugal, Porto, Portugal, acortereal@porto.ucp.pt

Cosme Almeida*, Catholic University of Portugal, Porto, Portugal, cealmeida@porto.ucp.pt

Pedro Veloso, Catholic University of Portugal, Porto, Portugal, pedro.veloso@wisemix.pt

ABSTRACT

The purpose of this paper is to develop an exclusively stakeholder-based financial brand

valuation approach.

A semiotic model is used that recognizes three components in the brand: identity, object and

response. It is noted that the financial valuation purpose is to predict the influence of brand

identity signs – the protectable trademarks as property rights – on the economic benefits of

their owners. These benefits depend on the response of the stakeholders who are generators

of cash-ins and cash-outs. In order to separate the "trademark influence", stakeholders are

confronted with a change scenario to a trademark that is unknown to them, and asked if this

change alters their behavioral response towards the brand. The affective response is also

evaluated to establish the "influence of risk" in realizing the future benefits.

This approach makes it possible to transform a rigorous concept from a legal and financial

point of view, but one which is incomprehensible to the common stakeholder, to a scenario

that the stakeholder can understand and respond to reliably.

Grounding the brand's financial valuation in semiotics is relevant because it distinguishes

legal, marketing and finance perspectives about the same objective, by framing them in

common concerns of objectivity and intelligibility.

Key Words: Brand, Equity, Valuation, Financial value, Marketing value, Semiotics.

INTRODUCTION

The purpose of this article is to substantiate a brand marketing valuation that provides the

necessary information for its subsequent financial valuation. The starting points for the

proposed approach are:

Based on the legal definition, which defines "brand" as a "sign", and in semiotics, the

"science of signs", the authors have determined three components: identity, object and

response (Lencastre and Côrte-Real 2010);

Based on the regulatory standardization of financial brand valuation, which defines

brand as an "intangible asset" (ISO 2010), the authors explain that for financial

valuation they are only considering the brand identity component, i.e. its set of

"trademarks” – name, logo, etc. – registrable and protectable as intellectual property

rights (WIPO 2017).

Indeed, for finance, an asset is a patrimony that generates future economic benefits for the

owners who possess and control it (IFRS 2004). It presupposes a right of ownership.

Being an intangible asset, that is to say without physical existence, it should be separable

(IFRS 2004), so one needs to be able to separate the economic benefits that are due to it. This

is the authors’ first concern – How can one autonomize the "trademark influence"?

A brand brings future economic benefit, but there is an inherent risk in forecasting those

benefits, which will be reflected in the rate at which they are currently discounted. It is

assumed that the risk will be smaller the greater the marketing value of the "brand" seen

holistically. This is the second concern – How can one calculate the "risk influence"?

It is assumed that the valuation should be based exclusively on the response of the actual and

potential stakeholders directly involved in generating economic benefits to the brand

(customers, suppliers, or in a broader sense users, benefactors, etc.). Valuations of other

audiences, possibly specialists, who are not directly involved in a monetary exchange

relationship (or estimated in monetary value) involving the brand, are avoided. Concerns

about the objectivity of the method, (even if there are difficulties arising from the natural

ignorance of the stakeholders), and about the complexity of the brand concept, underlie the

two questions formulated above.

Further worries about the objectivity of the method highlighted another problem about the

simplicity of the questions. In this article the authors make a very simplified simulation of a

questionnaire which was comprehensible to the respondents (without even mentioning the

word "brand", much less "trademark"). It intends to serve as a matrix for more complex

questionnaires that the rigorous demands of the financial valuation will impose. From a

marketing perspective, the trade-off between the detail of the information sought and the

understanding required by the respondent should not be overlooked.

BRAND AND TRADEMARK

Brand is a sign. In current and applicable language to the concept of brand, one can name its

three components as (1) the identity of the brand, (2) the object of the brand, and (3) the

response to the brand. Together they comprise the elements that underpin the concept of any

type of brand. This triadic decomposition of the sign, based on semiotics, integrates in a

single logic the multiplicity of the facets that make up the brand (Lencastre and Côrte-Real

2010). It allows us to locate and interrelate apparently disconnected brand approaches.

When looking at the brand as a semiotic triangle one can see that brand law focuses on

trademarks, i.e. the pillar of identity (the name McDonald's, the M logo on the golden arches,

or other less systematic identity signs, such as the Ronald McDonald mascot, or the current

slogan "I'm Lovin’ It"; what one can call the “identity mix” of the brand). Brand marketing,

on the other hand, focuses on the products and actions of sale/exchange, i.e. the pillar of the

object (the hamburgers, the stores, the advertising, the price; in general the “marketing mix”

of the brand). And finance focuses on stakeholder brand valuation, i.e. the pillar of the

response (sales, purchases, cash-flows; in short the economic benefits).

Legally, brand is a trademark, a sign of identity representing a property right that as such

should be regulated and protected (WIPO 2017). What is at stake is the distinctive capacity of

the trademark, so the main concern is its design and comparison with other signs that may

confuse the stakeholders.

In marketing, brand is much more than a trademark of identity, and the marketing tendency

has always been to subalternize the sign of identity in the strict sense of the law, and to

emphasize the object. The brand is a complex object, with products and actions of marketing

– marketing mix – whose meaning can go far beyond its physical or functional dimension,

taking on a specific guise by the person using it. But it is also marketing that highlights the

importance of signs in the strict sense – identity mix – as receptacles of the symbolic value

created around the object. And it is ultimately marketing that values the response to the signs.

Brand value (the “brand equity” in Farquhar's founding terminology in 1989, and generalized

by Aaker, since 1991, in marketing literature) evolved into a set of variables linked to

customers' cognitive, affective, and behavioral responses to identity mix and marketing mix

(Keller 1993; Yoo et al. 2000; Veloutsou et al. 2013). This set of variables can be called the

“response mix” of the brand.

The financial perspective runs in tandem with marketing to evaluate brand response (Simon

and Sullivan, 1993; see comparative evolution of the two perspectives in Davcik et al. 2015).

But, if marketing’s focus is on the customer or brand user, finance’s focus is on the brand

owner. Finance sees brand as an asset, in the sense that it is a patrimony that generates future

economic benefits for its owners (IFRS 2004). It is therefore from the owner’s perspective

that the brand is financially evaluated (ISO 2010). And the responses of the remaining

stakeholders, users or suppliers, are the sources of this value. It is this focus on the legal

ownership of the brand, its registrable and protectable signs, that concerns finance. Because,

in fact, what is at stake is to evaluate the trademark independent of its object and to monitor

the return on investment made therein, for example, in the case of a restyling, or when the

trademark is transacted alone, and is separated from the other assets of the entire business

(Bahadir et al. 2008; Machado et al. 2012). This value, being a semiotic artificiality (a sign is

an holistic and interactive entity), needs to be estimated for economic and commercial

reasons.

This relationship is demonstrated in Figure 1 (adapted from the brand model developed by

Lencastre and Côrte-Real 2010). The main problem that arises in the financial brand

valuation is that the brand is not being evaluated as a whole, with all its tangible and

intangible assets, but only with its legally protectable (TM) and registrable (®) signs. That is, in a given transaction of a product or service identified with the brand name, how much of the

amount paid relates to the brand identity and how much does it relate to its object?

Fig. 1 The semiotic brand triangle and the issue of financial valuation (Lencastre and Côrte-

Real 2010, adaptation)

For simplicity, the authors use the term "trademark" in subsequent text, whenever they mean

the legally protected and legally registered signs of brand identity. It is the intangible assets

that are being evaluated. They use the term "brand" whenever they mean not only the signs

of identity, but also the object and the response to the brand. The “trademark value” is the

value of the identity signs. It is a part of the “brand value”. The “brand value” is the value of

the entire business, identity, object and response.

TRADEMARK INFLUENCE

The share of profit attributable to the trademark may result from the differential price and/or

the differential quantity transacted that its presence causes in a stakeholder’s behavior. This

leads to the question of how to obtain the answer without placing the respondent in an

abstract situation, such as: “When you buy 100 units of this brand, how much do you buy

because of the product and how much do you buy because of the trademark?”; “When you

pay a price of 10 for a unit of this brand, how much do you pay for the product and how

much do you pay for the trademark?”. The situation gets even more complicated if one wants

to go further by analyzing other variables of the marketing mix: i.e. “When you use a certain

place to buy products of this brand how much is bought for the convenience of the place and

how much is bought because of the trademark?” Questions like these highlight (and are

substantiated with evidence) the artificiality of the analysis.

The problem has usually been solved by comparing the hypothetical situation of the

transaction being made without a trademark, i.e. without the presence of a name at the very

least. This solution is clear in theory but difficult to apply. What is a transaction without the

brand name? There is almost always a name to guarantee the transaction, even if it is the

identity of the seller. Is it not better to admit that it is an unknown name, without any mental

associations on the part of the buyer? This is the problem with which the authors are

presented. The questionnaire option to obtain the portion of value attributable to the brand

identity is: “Do you buy products from this brand?”; “If this brand changes the name to a

name unknown to you, do you continue to buy/not buy products from this brand?”; “How

much?”; “At what price?” It is obvious that the higher the preference for a brand that one

buys, the less will be the purchase intention if the brand changes identity (see research on this

situation of purchase intention in Delassus and Descotes, 2012; Round and Roper, 2015).

RISK INFLUENCE

The second element of marketing analysis required for financial valuation is connected to the

greater or lesser risk that is attributed to the brand in its ability to generate future economic

benefits.

Here one can make the link between the marketing value of the brand, which is viewed as a

whole, as an entire object, its multiple stakeholders and their respective responses, and

contrast that with the financial value of the trademark, which is seen as the owner’s asset.

One can and should calculate the marketing value of the brand – from its associations – in

comparison with the brands judged as competitors by its stakeholders (Fishbein 1963; Pulling

et al. 2006; Lencastre and Côrte-Real 2013). The comparison can be quantified in cognitive,

affective and behavioral response variables. The cognitive and affective responses are

predictors of the compartmental response. Awareness is usually considered the most

elementary necessary condition of brand value (Keller 1993). The preference can be

considered as the variable that most determines the purchase decision and consequently the

prediction of brand value (Cobb-Walgren et al. 1995).

From this comparison a risk indicator may result, which will affect the discount rate of future

benefits. For financial valuation, this brand risk indicator should take the form of a multiplier

which increases or decreases the discount rate corresponding to an average risk. The average

recommended risk rate (ISO, 2010) is the weighted average cost of capital (WACC) of the

industry where the brand is located (in case the brand object includes more than one activity,

one must consider different WACCs corresponding to the average risks of each activity).

MARKETING BRAND VALUATION

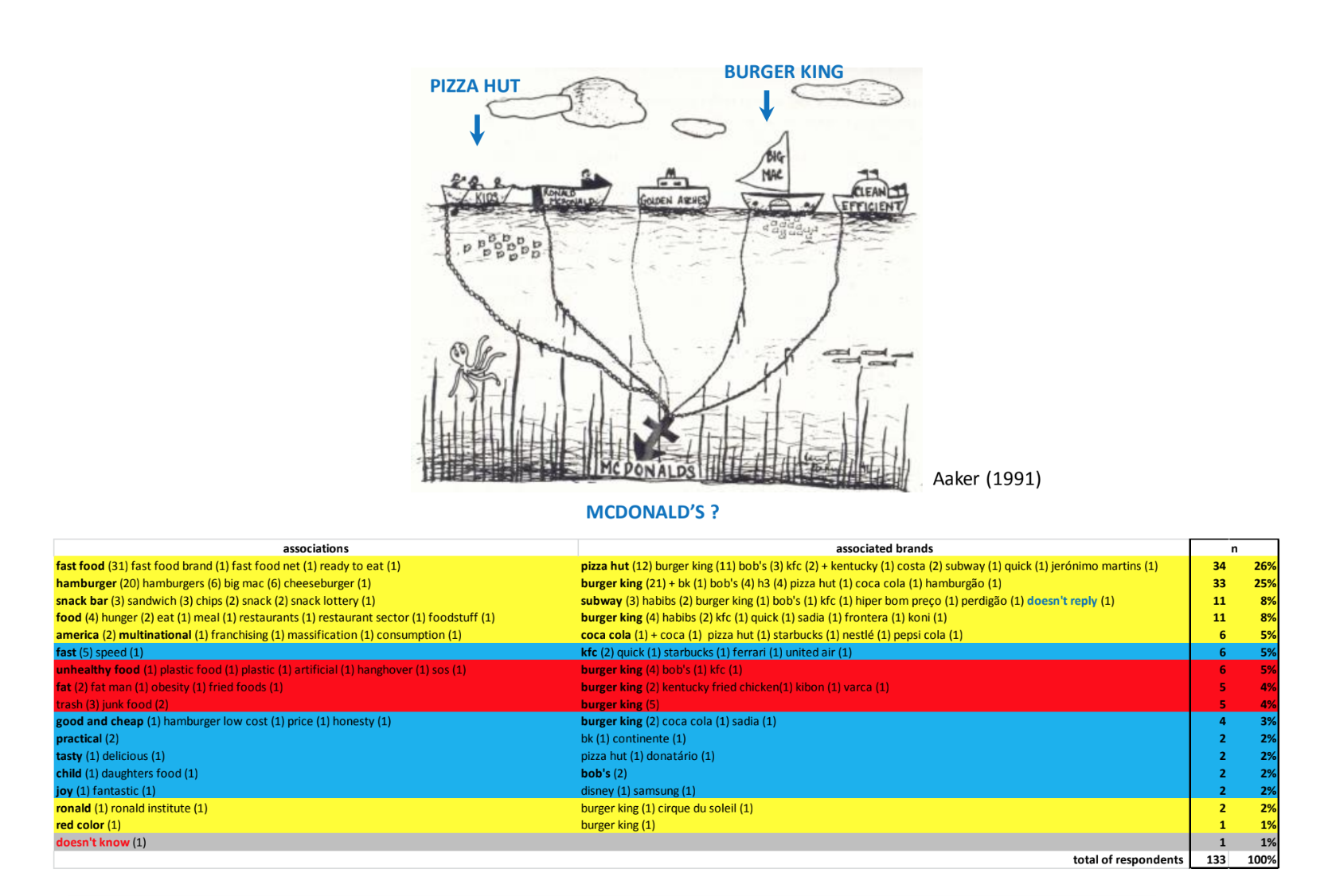

As a symbolic starting point one can look at Aaker's (1991) drawing in his book that

revolutionized the way that brand and brand value was regarded.

In Figure 2 this drawing is placed side by side with the results of a survey of potential

customers of the brand, in which they are asked:

(1) "Do you know McDonald's?" (If the answer was "yes"...)

(2) "With what word or short phrase do you associate McDonald's?"

(If the answer was "fast food"...)

(3) "What other fast food do you know?"

In the table of Figure 2 the authors transcribed all the associations obtained (organizing them

by themes), all the mentioned brands, and the frequency with which associations and brands

were cited. Yellow, blue and red colors were used to qualify, as neutral, favorable or

unfavorable, the associations obtained. The "n" column quantifies the brand awareness for

each association.

Fig. 2 McDonald's associations: (a) Aaker (1991, 64) with adaptions in blue and (b) results

from an inquiry into a convenience sample of 133 people, performed in Brazil and Portugal,

in 2016.

To quantify information about the affective and behavioral response to the brand, the authors

also asked the same respondents the next three questions:

(If the answer to question 3 was "Burger King"...)

(4) "Which one do you prefer McDonald's or Burger King?"

(5) "Do you buy McDonald's?"

(6) "Do you buy Burger King?"

In Appendix 1 the results of the given answers are presented. The "p" and "u" columns give

preference and use (the purchase in this specific case) of McDonald's for each association

obtained. It is with these values that the matrix of Figure 3 is constructed. Each association is

represented in function of its level of awareness (diameter of the circle); and in function of

the differentials of preference (abscissa) and use (ordinate) of McDonald's in relation to the

brands with which it shares the association. The differential values of preference and use are

calculated in Appendix 2 (columns Δp and Δu).

One can begin by looking at the brand holistically. It is located in the lower left quadrant of

the matrix of Figure 3, the red quadrant, negative in preference and in use (– 4% and –9% as

can be read in the total value of Table A2).

The analysis of this result is based on the associations that the brand has in the minds of the

respondents. As in a “psychoanalysis” of this brand “personality”, one can say that the brand

is penalized by its stronger association, "fast food", which is in the red quadrant (–12% in

preference and –15% in use). And that is valued by its other strong association, "hamburger",

more at the level of preference (+27%), less at the level of use (–3%), which is thus located in

the lower right quadrant – the blue quadrant – positive in preference, but still negative in use.

The remaining associations are much less strong in the sample survey (“snack bar”, “food”,

“American multinational”, “fast”, “unhealthy food”, etc.). As in the results of a focus group,

one can use these less frequent associations to imagine, or avoid, new strategies for the brand

(for instance in the case of future brand extensions).

The goal of the second matrix in Figure 3 is to show a direct comparison with the associated

brands. Its first great advantage is that it visually demonstrates the strength of the association

with each brand, and how competitive they are with McDonald's. Burger King, the biggest

competitor, has a slight shift in its favor to the right (preference +7%) and up (use +4%,

according to values Δ'p and Δ'u in Appendix 2). Pizza Hut is in the same situation, with a

sharper advantage. Bob's, the local Brazilian brand of hamburgers, is the only big competitor

to lose to McDonald's. As for the lesser evoked brands concentrated on the upper right

quadrant – the green quadrant – they are generally in a favorable position to McDonald's in

this survey.

In the simplest terms, this is a possible brand marketing valuation. It qualitatively evaluates

the brand from the associations that it awakens in the minds of its stakeholders, and quantifies

this valuation, by comparison with the competition, at different levels of response: cognitive,

affective and behavioral.

MARKETING INFORMATION FOR FINANCIAL BRAND VALUATION

In Appendix 1, in addition to the columns dedicated to awareness ("n"), preference ("p") and

use ("u"), there is a fourth column ("u0") that has not yet been analyzed. It results from the

answer to two additional questions arising from the simplified inquiry about McDonald's:

(7) "If McDonald's changes its name to an unknown name would you continue to buy/

not buy?" (According to the answer to question 5)

(8) "If Burger King changes its name to an unknown name would you continue to buy/

not buy?" (According to the answer to question 6)

Questions 7 and 8 were asked in order to simplify the difficult question of how to evaluate

the "influence of trademark" (this example is restricted to the brand name). And, contrary to

questions 5 and 6, which ask about current behaviors, questions 7 and 8 seek a conative

response, i.e. an intention of future behavior.

The formulation of the two questions is based on the assumption that the value of a trademark

results from the comparison between the value of the transaction of a product with the

trademark, and its hypothetical value without a trademark. As this situation is quite

unrealistic in most contemporary markets, it presents the scenario of change to an unknown

trademark, which is more understandable for the respondent.

Appendix 1 demonstrates that the differential between those who buy (59%, column "u") and

those who would buy if McDonald's changed its name (44%, column "u0") represents the

influence of the brand name on this sample market (59% – 44% = +15%). Appendix 2

calculates this differential for each of the associations (ΔTM column, differential purchase

with and without trademark, i.e. "trademark influence"). Very different situations are found

here: for example, the group which associate McDonald's with "hamburger" value the brand

name much more than the group which associates McDonald’s with “fast food” (+33% vs.

+9%). How does one interpret these new results in light of the brand valuation advanced so

far?

Fig. 3 McDonald’s response matrix of preference and use, with information on "trademark

influence" (ΔTM) and "risk influence" (Mβ) (Tables A1 and A2 from Appendix 1)

the risk?

FINANCIAL BRAND VALUATION

The matrix of preference and use of Figure 3, and the information that has been added about

the influence of trademark and risk, is intended to be a very simplified presentation of

marketing information collected for financial brand valuation. How, from these results, can a

financial value be reached?

In a subsequent article the authors will develop this point. Here, in order to clarify the

proposed approach, they can simulate a rapid exercise. Imagine that for the market

represented by this sample the accounting information indicates an annual cash-flow for the

brand of 100 million monetary units. Let's also imagine that the WACC of the brand industry

is 10%. If the trademark influence is ΔTM = +15%, then the annual cash-flow differential will

be 15 million. If the risk multiplier is Mβ = 1.19, the cash-flow discount rate will be 11.9%.

If, for lack of additional data on the future, the cash-flow of 15 million at the rate of 11.9% is

simply discounted as an annuity, then the value of the trademark will be 15 million / 11.9% =

126 million monetary units.

Obviously, this value is just one of many possible answers. Other scenarios, more optimistic

or more pessimistic, can be considered. First of all, it is necessary to differentiate non-

customers and customers (question 5), by using the calculation from the values obtained for

customers, since they are the ones who really contribute to the current cash-flows. One must

also distinguish between those who buy and stop buying (positive influence of trademark),

and those who do not buy and would buy if the brand changed its name (negative influence of

the trademark). The analysis can be expanded by undertaking financial valuation of the brand

in its multiple associations (that is, a “financial psychoanalysis"; for example, it has already

been noted that the value of the brand for those who associated it with "hamburgers" is higher

than for those who associated it with “fast food”).

CONCLUSION

The authors have presented a simplified exercise which demonstrates the link between the

marketing valuation and the financial valuation of a brand. They have previously tried to base

their work on semiotic assumptions – that brand is a “sign”. This is the most basic common

denominator of the different views on the brand; namely the law, marketing and finance – the

disciplines that are most involved in ascertaining financial valuation.

Simplicity is about intelligibility, but it must not mean lack of depth. It is possible, and

necessary, to deepen the presented approach.

Regarding identity, one should not just stick to the name, as other trademarks (logo, slogan,

and mascot, just to mention the most common) can be evaluated.

With regard to the object, one cannot confine one’s self to the exchange relationship of the

final product with the customer, which generates cash-ins, but must also consider exchange

relationships, of human and material resources, with other stakeholders, generating cash-outs.

As for the response, the sign component that the authors are evaluating, has endless

complexity, and just a few of the solutions they are working on, are listed below:

The behavioral response must quantify and deconstruct the variations of cash-flows

with and without trademark: “How much would you buy, less or more?”; “Is the

variation due to the price you would be available to pay or the quantity you would

buy?”. The goal is to try to infer the future as rigorously as possible. One can use not

only the behavior intentions stated by the respondents (conative response), but also

the extrapolation of their past behaviors (simulated behavioral response, obtained, for

example, using chains and transition matrices of Markov, 1971).

The affective response can also be enriched. The understanding of global preference

can be analyzed by inquiring and evaluating the different drivers of choice of brands

and making their assignment brand to brand (in accordance with Fishbein's theory of

reasoned action, 1963).

The cognitive response itself has variants (for example, spontaneous or assisted) that

may be more or less pertinent due to the nature of the industry, their stakeholders and

their respective exchange relationships. The adequacy of the questionnaires to the

profile of the different stakeholders is a key point of the authors’ approach.

1 The respondents were postgraduate students (Master of Science, MBA and postgraduate

courses) from the business schools of the Catholic University of Portugal, in Porto, and

Pontificial Catholic University of Rio de Janeiro (Brazil). Quota sampling was used, with an

equal number of respondents from each University (n = 66 x 2 = 132). For didactic reasons of

results presentation, the authors created an additional respondent (n = 133) who said that he

didn’t know McDonald’s (question 1), and so that respondent was excluded from the rest of

the questionnaire. Because it is an exploratory study, the authors preferred to administer the

questionnaire face to face in order to detect the respondents’ difficulties to the questions. The

questionnaire was in Portuguese, which was the native language of most of the respondents.

Appendix 1 McDonald’s associations: inquiry to a convenience sample of 133 people,

performed in Brazil and Portugal (2016)

Appendix 2 McDonald’s associations: the differential response of preference (Δp) and use

(Δu), and the influence of trademark (ΔTM) and risk (Mβ)

Differences in Appendix 2 in relation to some of the values in the source table of Appendix 1

are due to rounding (for example in Appendix 1 the association "hamburger" is u = 79% and

u0 = 45%, as such a difference is of 79% – 45% = +34%, and in Appendix 2 appears u-u0 =

+33%).

References

Aaker, D.A. (1991). Managing Brand Equity: Capitalizing on the Value of a Brand Name.

New York: The Free Press.

Bahadir, S. C., Bharadwaj, S. & Srivastava, R. (2008). Financial value of brands in mergers

and acquisitions: Is value in the eye of the beholder? Journal of Marketing, 72, 49-64.

Cobb-Walgren, C. G., Ruble, C. A. & Donthu, N. (1995). Brand equity, brand preference and

purchase intent. Journal of Advertising, 24, 3, 25-40.

Davcik, N. S., Vinhas da Silva, R. & Hair, J. F. (2015). Towards a unified theory of brand

equity: Conceptualization, taxonomy, and avenues for future research. Journal of Product

and Brand Management, 24, 1, 3-17.

Delassus, V. P. & Descotes, R. M. (2012). Brand name substitution and brand equity transfer.

Journal of Product and Brand Management, 24, 1, 28-42.

Farquhar, P.H. (1989). Managing brand equity. Marketing Research, 1, 24-33.

Fishbein, M. (1963). An investigation of the relationship between beliefs about an object and

the attitude toward that object. Human Relations, 16, 3, 233-239.

International Financial Reporting Standards Foundation – IFRS Foundation (2004).

Intangible Assets. International Accounting Standard IAS 38.

International Organization for Standardization – ISO (2010). Brand Valuation: Requirements

for Monetary Brand Valuation. International Organization Standard ISO 10668.

Keller, K.L. (1993). Conceptualizing, measuring and managing customer-based brand equity.

Journal of Marketing, 57, 1-22.

Lencastre, P. & Côrte-Real, A. (2010). One, two, three: a practical brand anatomy. Journal of

Brand Management, 17, 6, 399-412.

Lencastre, P. & Côrte-Real, A. (2013). Brand response analysis: A Peircean semiotic

approach. The Journal of Social Semiotics, 23, 4, 489-506.

Machado, J.C., Carvalho, L.V., Costa, P. & Lencastre, P. (2012). Brand mergers: Examining

consumers’ responses to name and logo design. Journal of Product and Brand Management,

21, 6, 418-427.

Markov, A.A. (1971). Extension of the limit theorems of probability theory to a sum of

variables connected in a chain. In R. Howard, Dynamic Probabilistic Systems (Appendix B of

Vol. 1). New York: John Wiley and Sons.

Pulling, C.P., Simmons, C.J. & Netemeyer, R.G. (2006). Brand dilution: When do new

brands hurt existing brands? Journal of Marketing, 70, 52-66.

Round, G. & Roper, S. (2015). Untangling the brand name from the branded entity. European

Journal of Marketing, 49, 11/12, 1941-1960.

Simon, C. & Sullivan, M. (1993). The measurement and determinants of brand equity: A

financial approach. Marketing Science, 12, 1, 28-52.

Veloutsou, C., Christodoulides, G. & de Chernatony, L. (2013). A taxonomy of measures for

consumer-based brand equity: Drawing on the views of managers in Europe. Journal of

Product and Brand Management, 22, 3, 238-248.

World Intellectual Property Organisation – WIPO (2017). What is Intellectual Property?

Retrieved September 15, 2017 from http://www.wipo.int/about-ip/en/

Yoo, B., Donthu, N. & Lee, S. (2000). An examination of selected marketing mix elements

and brand equity. Journal of the Academy of Marketing Science, 28, 2, 195-211.